The second week of 2025 witnessed a series of transformative regulatory developments across diverse financial domains. From advancements in reporting standards to reinforced compliance requirements, these updates reflect the evolving priorities of regulators and institutions in addressing risks, enhancing transparency, and fostering resilience in the financial ecosystem. The focus on digitalization, sustainability, and cross-border harmonization signals a global commitment to aligning regulatory frameworks with modern challenges and opportunities.

Business Line | Country | Regulator | Regulatory Update | Summary |

All | British Virgin Islands | BVIFSC | The British Virgin Islands (BVI) has introduced the Financial Services (Miscellaneous Exemptions) (Amendment) Regulations, 2024, effective retroactively from October 15, 2024. The amendment, published on December 4, 2024, exempts specific categories of licensees—including private funds, professional funds, public funds, and approved investment managers—from seeking prior approval from the Financial Services Commission for appointing Money Laundering Reporting Officers (MLROs). However, these entities are required to notify the Commission within 14 days of such appointments. The amendment further clarifies that the exemptions do not absolve licensees of their regulatory responsibilities regarding compliance and money laundering reporting. This regulatory update aims to streamline administrative processes while maintaining robust compliance obligations. | |

British Virgin Islands | BVIFSC | The British Virgin Islands (BVI) has implemented the Anti-Money Laundering (Amendment) Regulations, 2024, gazetted on September 6, 2024. These amendments, enacted under the Proceeds of Criminal Conduct Act, reinforce the duties and qualifications of Money Laundering Reporting Officers (MLROs). Relevant persons must now appoint MLROs with adequate qualifications, experience, and seniority, ensuring they are fit and proper under stringent criteria. Appointments require prior approval from the Financial Investigation Agency or Financial Services Commission, depending on the entity type. The regulations also enhance the supervisory framework, granting authorities the power to suspend or withdraw approvals for MLROs under specific circumstances, such as misconduct or non-compliance. These updates aim to bolster the Territory’s defences against money laundering, terrorist financing, and proliferation financing while aligning with international standards. | ||

European Union | EBA | Enhanced Guidelines for Managing ESG Risks in Financial Institutions | The European Banking Authority (EBA) has released comprehensive guidelines to strengthen the management of environmental, social, and governance (ESG) risks within financial institutions. These guidelines mandate institutions to integrate ESG risks into their core risk management frameworks, addressing short-, medium-, and long-term impacts across various categories of financial risks, such as credit, market, operational, and reputational risks. Institutions are required to adopt methodologies like exposure-based, portfolio-based, and scenario-based analyses to effectively assess ESG risks. Moreover, robust data processes, alignment with regulatory objectives like the EU Climate Law, and detailed transition planning are essential components of these new measures. The guidelines emphasize internal governance, risk appetite adjustments, and continuous monitoring, while also setting clear compliance timelines, effective January 2026 for large institutions and January 2027 for smaller entities | |

European Union | EBA | Draft Regulatory Standards on Crypto-Asset Exposures Under CRR Article 501d(5) | The European Banking Authority (EBA) has issued a consultation paper on draft Regulatory Technical Standards (RTS) for the calculation and aggregation of crypto-asset exposures under Article 501d(5) of the Capital Requirements Regulation (CRR). These standards aim to establish clear guidelines for the prudential treatment of crypto-asset exposures, ensuring consistency with the Basel Committee standards and the EU’s Markets in Crypto-Assets Regulation (MiCAR). Key proposals include specifying capital treatment for various crypto-asset categories, integrating risk-sensitive approaches for credit and market risks, and setting valuation criteria to address the volatility and transparency challenges of crypto-assets. The draft RTS will serve as transitional measures until the full implementation of permanent prudential frameworks, with significant implications for credit institutions managing crypto-assets. Feedback on the consultation is invited until April 2024 | |

European Union | European Union | The European Union has introduced Directive (EU) 2025/50 to enhance the efficiency and security of withholding tax relief procedures on cross-border dividends and interest payments. Aimed at supporting the Capital Markets Union (CMU), the directive mandates the adoption of a digital tax residence certificate (eTRC) and harmonizes relief systems, such as relief-at-source and quick refund mechanisms. Financial intermediaries must register on national certified registers, comply with reporting obligations, and provide detailed information about payment chains and beneficiary eligibility. Anti-abuse measures, including checks on financial arrangements and holding periods, are integrated to prevent tax fraud and evasion. Member States are required to implement these rules by January 1, 2030, ensuring uniformity and transparency across the EU’s financial markets. | ||

Finland | FSA | The Financial Supervisory Authority (FIN-FSA) issued updated regulations and guidelines (4/2023) aimed at improving compliance with sanctions regulation and national freezing orders. Effective from March 1, 2024, these measures mandate supervised entities, including financial institutions and crypto-asset service providers, to adopt comprehensive IT systems for sanctions screening. The regulations emphasize customer due diligence, risk-based assessments, and robust internal controls to ensure adherence to sanctions. Key enhancements include obligations for regular system testing, reporting of incidents, and the use of advanced techniques such as fuzzy logic to detect variations in sanctioned party names. These updates align with EU Best Practices on Sanctions and aim to bolster safeguards against sanctions evasion and financial crime. | ||

Global | BIS | The BIS Committee on Payments and Market Infrastructures (CPMI) has announced key initiatives to promote the harmonisation of ISO 20022 data requirements for cross-border payments, aiming to enhance efficiency and security. To ensure medium-term governance and maintenance, CPMI will establish a global panel of ISO 20022 market practice groups in early 2025, with semi-annual meetings aligned with ISO 20022 standards. This initiative supports the G20 cross-border payments program and will remain active until at least 2027. Additionally, CPMI is driving industry-led efforts to develop global ISO 20022 market practice guidelines for fast payments, including the relaunch of the Instant Payments Plus (IP+) group. These measures are expected to accelerate the global adoption of harmonised ISO 20022 standards, paving the way for safer and more efficient cross-border payment systems. | ||

Indonesia | OJK | The Financial Services Authority of Indonesia (OJK) has issued significant new regulations to enhance the governance and oversight of digital finance and cryptocurrency markets. Among the initiatives, POJK 27/2024 and SEOJK 20/2024 establish detailed frameworks for the licensing, reporting, and monitoring of digital assets and crypto operations, set to take effect on January 10, 2025. These rules aim to strengthen transparency, consumer protection, and risk management in a rapidly growing sector. Additionally, OJK launched measures to promote inclusivity, such as introducing accessibility guidelines for financial services targeting individuals with disabilities. These reforms underscore Indonesia’s commitment to fostering a secure, inclusive, and sustainable financial ecosystem while aligning with global best practices in digital asset regulation. | ||

Luxembourg | CSSF | Luxembourg Adopts CSRD and ESRS for Sustainability Reporting | Luxembourg’s CSSF has highlighted the application of the Corporate Sustainability Reporting Directive (CSRD) and European Sustainability Reporting Standards (ESRS), which require eligible investment fund managers (GFI) and registered alternative investment fund managers (GFIA) to comply with enhanced sustainability reporting obligations. Effective January 1, 2024, with the first reports due in 2025, these regulations apply to entities organized under specific legal forms (e.g., SA, SARL, SCA) and classified as large enterprises exceeding thresholds for total assets (€25 million), net turnover (€50 million), or employee count (250). Exemptions are available for non-listed subsidiaries included in consolidated reports of EEA parent companies. Entities must evaluate their eligibility and align their practices with the updated requirements, leveraging available support programs for compliance. | |

Malta | MFSA | Enhanced Climate and Environmental Risk Management in Maltese Banks | The Malta Financial Services Authority (MFSA) has issued a “Dear CEO” letter following its 2023/2024 Thematic Review on Climate-Related and Environmental (C&E) Risks. This initiative emphasizes the urgent need for Less Significant Institutions (LSIs) to strengthen their frameworks for identifying, managing, and mitigating C&E risks. The review identified progress in areas like materiality assessments and governance but highlighted gaps in aligning C&E risks with traditional financial risks, such as credit, operational, and market risks. The MFSA calls for comprehensive strategies, including robust risk quantification, scenario analysis, and integration into governance and remuneration frameworks. Maltese banks are required to submit a gap analysis and remediation plan by June 2025, aligning with upcoming EU and ECB regulatory expectations. | |

Malta | MFSA | The Malta Financial Services Authority (MFSA) has issued a consultation on the implementation of a new Crypto-Asset Service Provider (CASP) Return, applicable to entities licensed under the Markets in Crypto-Assets Act. The CASP Return is designed to enhance data collection and supervision of crypto-asset activities, featuring multiple reporting sheets such as income statements, balance sheets, custody details, and complaints. Reporting will commence from December 30, 2024, with obligations for quarterly returns, annual returns, and audited returns to ensure compliance. The CASP Return also integrates validation mechanisms for data consistency and supports multi-currency reporting. Stakeholders are invited to provide feedback on this proposal by January 31, 2025, to help shape the final framework. | ||

United Kingdom | BOE | The Financial Conduct Authority (FCA) and Prudential Regulation Authority (PRA) have issued a consultation on the proposed Management Expenses Levy Limit (MELL) for the Financial Services Compensation Scheme (FSCS) for the 2025/26 financial year. The proposed MELL is set at £108.6 million, comprising a management expenses budget of £103.6 million and an unlevied reserve of £5 million. While the MELL reflects a nominal increase of £0.5 million compared to 2024/25, it is lower in real terms due to inflation absorption. The budget supports ongoing FSCS operations, including claims handling, IT improvements, and outsourcing reductions, with a shift toward in-house capabilities. Stakeholders can submit feedback until February 7, 2025, as the FCA and PRA aim to finalize rules by April 1, 2025. | ||

United Kingdom | FCA | The Financial Conduct Authority (FCA) has released a consultation paper outlining a proposed framework for “targeted support” aimed at helping Defined Contribution (DC) pension holders make better financial decisions. The initiative seeks to bridge the gap between holistic advice and generic guidance by offering tailored suggestions to pre-defined consumer segments, rather than fully personalized advice. The framework is designed to address challenges such as under saving for retirement and confusion around decumulation options. While targeted support is not bespoke, the FCA believes it can be scaled effectively to support a broader population. Stakeholder feedback is invited by February 13, 2025, to refine the framework and ensure alignment with consumer protection standards. | ||

Banking | Hong Kong | HKMA | The Hong Kong Monetary Authority (HKMA) has launched the Supervisory Incubator for Distributed Ledger Technology (DLT) to promote the responsible adoption of DLT within the banking sector. This initiative aims to help banks maximize the benefits of DLT while effectively managing risks associated with integrating DLT-based solutions into traditional banking systems. The Incubator provides a one-stop supervisory platform where banks can validate risk management controls and conduct live trials under HKMA supervision before launching DLT-driven services like tokenized deposits. Additionally, it fosters industry awareness through supervisory guidance, industry sessions, and research projects to establish best practices for DLT adoption. Announced during FiNETech4, the Incubator represents HKMA’s commitment to driving safe and efficient innovation within the financial industry. | |

Nigeria | CAC | Corporate Affairs Commission Issues Guidelines for Bank Recapitalization | The Corporate Affairs Commission (CAC) of Nigeria has released comprehensive guidelines for the recapitalization of banks and other financial institutions, pursuant to Section 8 (1) (e) of the Companies and Allied Matters Act (CAMA) 2020. The guidelines cover processes such as new incorporations, increases in share capital (via private placements, rights issues, or subscriptions), mergers, and license upgrades or downgrades. For new incorporations, approvals from the sector regulator and completion of prescribed forms are required. In cases of increased share capital, regulatory approval and declarations by directors are mandatory. Mergers require a court-sanctioned scheme and publication in newspapers. The CAC assures a swift issuance of relevant certificates within 24 hours if requirements are met. Queries on these guidelines can be directed to the CAC via their official email. These measures aim to streamline regulatory compliance and ensure effective recapitalization within Nigeria’s financial sector. | |

United States | Department of the Treasury | The U.S. Department of the Treasury released a policy brief, Financing Small Business: Landscape and Recommendations, highlighting key trends, barriers, and recommendations for enhancing small business financing. The brief identifies challenges faced by small business owners, including difficulty in comparing financial products and accessing capital, especially for underserved communities. It underscores the growing role of fintech in the small business lending landscape amidst tightened bank credit standards. Recommendations include fostering uniform disclosure standards across financing products to enhance transparency, leveraging government programs like SBA initiatives, and improving interagency coordination to support small business financing. The Treasury emphasizes the need for regulators to address the risks and opportunities posed by emerging technologies, such as AI, in small business lending. These efforts aim to create a competitive, inclusive financial ecosystem that supports the diverse needs of small businesses. | ||

Insurance | Canada | FCNB | CCIR and CISRO Propose Consolidated Segregated Funds Guidance | The Canadian Council of Insurance Regulators (CCIR) and the Canadian Insurance Services Regulatory Organizations (CISRO) have released a proposed Consolidated Segregated Funds Guidance for public consultation. This guidance aims to standardize expectations for insurers and intermediaries regarding the design, sale, and servicing of individual variable insurance contracts (IVICs). Key components include “know your customer” and “know your product” requirements, robust controls around sales charge options, ongoing disclosure requirements, and corporate governance standards. This initiative addresses gaps in conduct standards, ensuring fair treatment of customers compared to mutual funds. Public comments are invited until April 8, 2025. The guidance represents a collaborative effort to establish a consistent national standard across Canadian provinces and territories. |

European Union | European Union | Introduction of the EU Recovery and Resolution Framework for Insurance Undertakings | The European Union has introduced Directive (EU) 2025/1, establishing a comprehensive framework for the recovery and resolution of insurance and reinsurance undertakings. This directive aims to address vulnerabilities in the insurance sector by ensuring financial stability, minimizing the impact of failures, and safeguarding policyholders’ interests. It builds upon existing frameworks such as Solvency II, introducing pre-emptive recovery planning and resolution tools to manage distressed undertakings effectively. Key features include group-level resolution planning, mechanisms for ensuring the continuity of critical functions, and enhanced cross-border coordination among resolution authorities. The directive also mandates the development of insurance guarantee schemes to provide financial protection to policyholders and promote trust in the internal insurance market across EU Member States. | |

European Union | European Union | Enhancing Proportionality and Sustainability in Insurance Regulation | The European Union has adopted Directive (EU) 2025/2, amending Directive 2009/138/EC (Solvency II) to address proportionality, sustainability, and macro-prudential supervision within the insurance and reinsurance sectors. This update introduces streamlined requirements for small and non-complex undertakings, allowing for proportional reporting and governance adjustments, thereby reducing compliance burdens. The directive also integrates climate change risk assessment through mandatory scenario analysis and strengthens the role of macro-prudential tools to enhance financial stability. Additionally, it emphasizes the insurance sector’s role in supporting the EU’s sustainability goals, with specific measures to manage environmental risks and promote green finance initiatives. Enhanced cooperation among supervisory authorities aims to ensure uniformity and robust cross-border oversight. | |

Indonesia | OJK | New Reporting Requirements for Insurance and Pension Sectors | The Indonesian Financial Services Authority (OJK) has issued two new regulations aimed at enhancing transparency, efficiency, and accountability in reporting by the insurance and pension sectors. Regulation No. 21/2024 mandates pension funds to submit periodic reports, including monthly financial statements and annual audited reports, through OJK’s online system. Transparency is further emphasized by requiring reports to be accessible to participants. Meanwhile, Regulation No. 22/2024 revises reporting standards for insurance companies to align with the latest accounting standards for insurance contracts, effective January 2025. This regulation introduces stricter administrative penalties for late or inaccurate submissions, ensuring better compliance and supervision within the industry. These measures aim to bolster the reliability of financial disclosures and strengthen consumer protection in both sectors. | |

Investment | European Union | ESMA | The European Securities and Markets Authority (ESMA) has published the final report on its revised guidelines for stress test scenarios under the Money Market Fund (MMF) Regulation. The updated guidelines incorporate changes to risk parameters reflecting current market dynamics and emerging risks, ensuring better preparedness for adverse scenarios. Key updates include adjustments to liquidity and credit risk parameters and methodologies for stress testing redemption pressure. These updates aim to enhance the resilience of MMFs and align them with evolving regulatory priorities in financial stability. The implementation date for these updated guidelines is outlined in the report, emphasizing the importance of timely compliance for fund managers. | |

Global | PRI Association | The Principles for Responsible Investment (PRI), in collaboration with UNEP FI and the Generation Foundation, has released comprehensive guidance on “Investing for Sustainability Impact” (IFSI), aimed at institutional investors including asset owners and managers. This guidance introduces a four-part framework to implement IFSI effectively, encompassing the determination of investor intentions, setting sustainability goals, taking impactful actions through capital allocation, stewardship, and policy engagement, and measuring progress against these goals. The guidance aligns sustainability impact with fiduciary duties and underscores its growing importance amid systemic risks like climate change and biodiversity loss. However, implementing IFSI presents challenges such as complex intermediation chains, misaligned incentives, and benchmarking limitations, for which the guide also proposes practical solutions. PRI encourages investors to review case studies and tools designed to demonstrate IFSI in practice. | ||

Guernsey | GFSC | The Guernsey Financial Services Commission (GFSC) has issued a consultation paper proposing revisions to the Prospectus Rules, aiming to streamline regulatory requirements while ensuring alignment with international standards. Key changes include expanding exemptions for promotions to “Professional Investors” and identifiable groups of up to 200 individuals, enhancing disclosure requirements for registered collective investment schemes, and formalizing practices for valuation, fees, and conflict-of-interest reporting. The rules also introduce clarifications on circulation procedures and notification obligations for prospectus amendments. These updates, reflecting feedback from industry stakeholders and IOSCO principles, are intended to modernize the regulatory framework and reduce administrative burdens. The consultation period ends on March 3, 2025. | ||

Luxembourg | CSSF | The Luxembourg Commission de Surveillance du Secteur Financier (CSSF) has introduced Circular CSSF 25/870, which revises the reporting requirements under Circular CSSF 24/853. The updated framework applies to all investment firms as of the financial year ending December 31, 2024, expanding the scope to include Partial Scope Investment Firms for select reports. Key elements include the mandatory submission of a digital Self-Assessment Questionnaire (SAQ) and enhanced reporting on anti-money laundering (AML/CFT) and MiFID compliance. While certain firms are exempt from submitting Agreed-Upon Procedure (AUP) reports initially, all are required to adhere to annual reporting on AML/CFT and the protection of client financial instruments. The changes align with CSSF’s risk-based supervision strategy and its push towards digitalized and efficient reporting processes. |

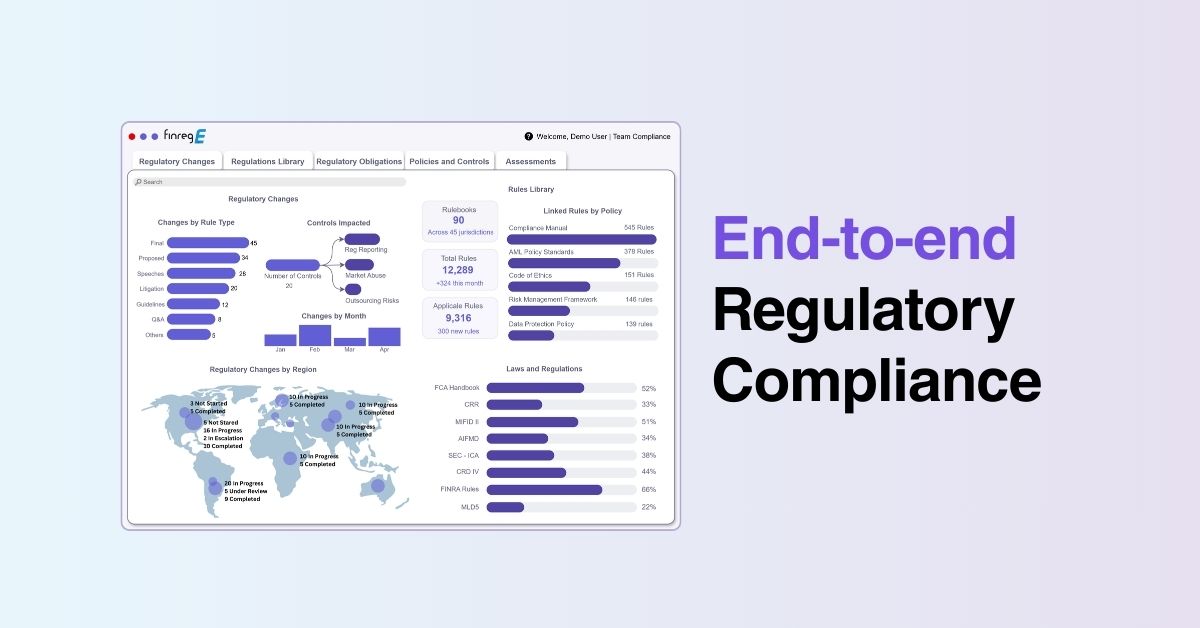

As regulatory landscapes continue to shift, staying ahead of compliance requirements becomes increasingly complex. FinregE and its AI-powered compliance management solutions simplify this challenge by providing robust tools for horizon scanning, real-time updates, and tailored insights. Whether it’s adapting to ESG mandates or managing cross-border reporting, FinregE empowers institutions to navigate regulatory changes with confidence, ensuring compliance and operational efficiency. Book a Demo today.